The Shrinking Public Market: Making Small Investors Losers

Over the past 20 years, a dramatic shift has been taking place in the capital markets. According to Pantheon, the number of publicly listed companies in the U.S. has declined by 50% since its peak in 1996. Previously, the average time for a company to IPO was 3-6 years. Now companies on average are staying private longer and having an IPO or M&A after 10-14 years. Private Equity firms like BlackRock and T. Rowe Price have found that by keeping these high growth companies private and injecting additional capital, they are able to make significant returns before the company IPOs at a much higher value. See below for an illustration.

Private equity has had average annual returns of 11.8% over the past 10 years.

So why doesn’t everyone invest in private equity if it has been proven to outperform the public markets?

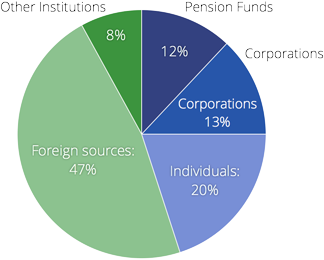

Unfortunately, only about 1% of the investing population has had direct access to private equity – institutional investors and ultra-high-net-worth individuals. Below is an illustration of the main sources of private equity money in Canada – who make up this tiny 1%.

Historically, only sophisticated investors have been able to invest in areas like private equity, venture capital, hedge funds, real estate, and other alternatives while retail investors are locked out due to higher minimum mandates and limited access. Retail investors primarily invest through defined contribution plans such as a 401(k), which rarely include the asset classes mentioned above, or charge exorbitant fees when they do.

Kevin Albert, a partner at Pantheon who leads business development and client service says “slow-growth companies are dominating the public markets. Returns from private equity and other investments are flowing to rich people. There’s a progressive argument here.” Is it fair that only the rich can access this superior asset class?

According to BCG’s 2017 wealth management report, portfolios of households with $20 million to $100 million grew almost twice as fast as those between $250,000 and $1 million. This excess return experienced by the ultra-rich was attributed to the liquidity premium – achieving better returns by allowing money to be locked up for extended periods of time, which, in most cases, is not possible for smaller portfolios and retail investors.

With the promise of higher returns, asset managers are scrambling to offer versions of private equity and other alternatives to retail investors. Brent Beardsley, Managing Director at BCG, emphasizes that individuals belonging to defined benefit pension plans have always benefited from alternatives and believes all investors should have the same opportunity.

Various factors have contributed to public companies’ thinning numbers. These include rising regulatory costs and the threat of activist investors, who often demand big strategy changes. Private companies used to go public to access capital for growth, but now they have the ability to stay private and raise money all the same. According to Institutional Investor, private equity firms possessed $1.5 trillion in assets in 2016, meaning no shortage for young companies seeking investment capital.

The shrinking public market is creating an environment where returns are becoming more and more difficult to generate. Institutional investors and high-net-worth individuals are outperforming retail investors because they are able to allocate portions of their portfolios to private equity. How much longer until private equity investments are available to all investors? You may be able to access high-growth private companies easier than you think.